Samuelson and Co - Revisiting the Relationship Between Equity and Commodity Markets: It's Complicated

Dec 7, 2024·

,

,

·

0 min read

,

,

·

0 min read

Sania Wadud

Robert B. Durand

Marc Gronwald

Abstract

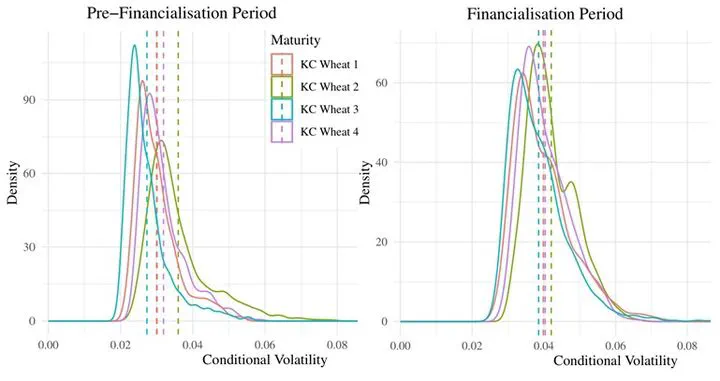

This paper analyzes commodity pricing within a unified framework that explores the interplay of (i) seasonality, (ii) the Samuelson maturity effect, (iii) the Samuelson correlation effect, and (iv) the increasing integration with equity markets. Key findings include: (1) index commodities exhibit higher volatility than off-index commodities, (2) financialisation reduces seasonality in price volatility for some index commodities, (3) while the Samuelson (1965) maturity effect—suggesting lower volatility in longer-dated contracts—persists, it has weakened since financialisation, and (4) no evidence of a Samuelson correlation effect between equity and commodity markets post-financialisation is observed.

Publication

Under review at the Journal of Empirical Finance